The 30% Valuation Gap: Why French TPM Businesses Trade at a Discount

9 June 2026 - 6 Minute Read

Understanding How Employment Laws Influence Third-Party Maintenance Valuations

The global Third-Party Maintenance (TPM) industry has undergone significant consolidation over the past decade, with private equity firms and strategic acquirers investing heavily in maintenance providers across North America, Europe, and Asia.

Yet not all TPM businesses attract the same valuation multiples.

From discussions Baby Blue has had with private equity investors, strategic acquirers, investment bankers and industry executives over the past 18 months, a recurring theme has emerged: French TPM businesses are often viewed as being worth approximately 30% less than comparable UK or US-based providers.

Whilst every transaction is unique and valuations are influenced by multiple factors, labour flexibility, restructuring costs and integration risk are consistently cited as major contributors to this valuation gap.

For many investors, the issue is not the quality of the business, its customers, engineering capability or market position. Rather, it is the cost, complexity and timescales involved in creating post-acquisition synergies.

Why Labour Flexibility Matters in TPM

The TPM sector is fundamentally a people business.

Unlike software companies, where revenue can often grow without significant increases in headcount, TPM providers rely heavily on:

- Field engineers

- Technical support staff

- Service delivery teams

- Logistics personnel

- Customer support functions

- Sales and account management teams

- Management and operational leadership

As a result, payroll is often one of the largest costs within the business.

When a TPM provider is acquired, buyers almost always identify opportunities to improve profitability through operational synergies.

These may include:

- Combining sales teams

- Consolidating service desks

- Merging finance and HR functions

- Rationalising warehouse operations

- Eliminating duplicate management positions

- Standardising operational processes

- Integrating systems and reporting structures

The speed at which these synergies can be delivered has a direct impact on investor returns.

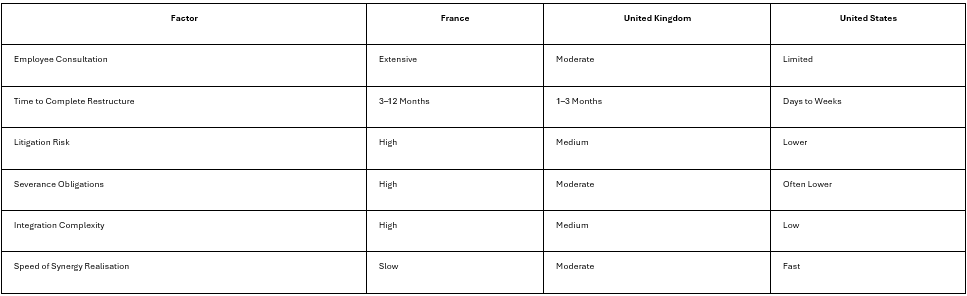

France: A Challenging Environment for Acquirers

France has some of the strongest employee protections in the developed world.

While these protections provide important security for workers, they can create significant challenges for investors seeking to restructure a business after an acquisition.

Typical challenges include:

- Extensive employee consultation requirements

- Mandatory involvement of employee representatives

- Higher severance obligations

- Increased legal and administrative complexity

- Greater risk of employment disputes

- Longer implementation times for organisational change

For larger restructuring programmes, consultation processes can extend for several months before any changes can be implemented.

It is not uncommon for acquirers to spend six months or more navigating employment procedures before achieving their desired organisational structure.

The result is delayed synergy savings, increased costs and lower investment returns.

The United Kingdom: Greater Flexibility

Historically, the United Kingdom has been viewed as one of Europe’s more flexible labour markets.

Employers must still follow fair and lawful processes, but the framework is generally less restrictive than that found in France.

Key characteristics include:

- Shorter consultation periods

- Faster decision making

- Lower legal complexity

- More predictable employment tribunal outcomes

- Greater flexibility when redesigning organisational structures

For many TPM acquisitions, restructuring programmes can often be completed within one to three months, allowing buyers to realise synergies significantly faster than in France.

The United States: Maximum Flexibility

The United States remains one of the most attractive labour markets from an investor’s perspective.

Many states operate under “at-will employment” principles, allowing employers to make organisational changes far more quickly than is possible across much of Europe.

Whilst employment laws still provide important protections, investors generally benefit from:

- Faster integration programmes

- Lower restructuring costs

- Reduced legal complexity

- Earlier synergy realisation

- Greater certainty of execution

These advantages frequently translate into higher acquisition multiples for US-based service businesses.

Typical Restructuring Comparison

The Synergy Challenge

In the TPM sector, acquisitions are rarely made simply to acquire revenue.

Buyers are typically purchasing customers, engineering capability, geographic coverage, technical expertise and market share.

The investment thesis almost always includes some level of synergy creation.

A typical acquirer may seek to:

- Consolidate finance teams

- Merge service desks

- Rationalise warehouses

- Eliminate duplicate management positions

- Combine sales and marketing functions

- Standardise operational processes

In the United States, many of these changes can be implemented within weeks.

In the United Kingdom, they may take several months.

In France, the same process can often extend significantly longer and involve substantial consultation, legal oversight and additional costs.

From an investor’s perspective, delayed synergies mean delayed returns.

If EBITDA improvements are pushed out by six, twelve or even eighteen months, the value of the acquisition falls accordingly.

This is one of the reasons investors frequently cite French employment legislation as a factor that suppresses valuation multiples compared with equivalent businesses in the UK and US markets.

Could the UK Become More Like France?

The UK has historically benefited from a reputation for labour market flexibility and a generally pro-business regulatory environment.

However, employment regulation is never static.

Across the political spectrum there is increasing debate regarding:

- Employee rights

- Unfair dismissal protections

- Flexible working requirements

- Collective consultation obligations

- Union influence

- Employer responsibilities

- Corporate taxation

Supporters of stronger employee protections argue that such measures improve fairness, job security and long-term economic stability.

Critics argue that excessive regulation can increase costs, reduce flexibility, discourage investment and make acquisitions less attractive.

Some investors are already questioning whether the UK could gradually move closer to the European employment model if future governments pursue significantly more interventionist labour policies.

This concern is particularly relevant given ongoing debates within the Labour movement regarding workers’ rights and employment reform. Should future leadership emerge from the more left-leaning wing of British politics, some investors fear that the UK could move further towards the French model of employment regulation.

Whether those concerns ultimately prove justified remains to be seen.

However, perception often influences investment decisions just as much as reality.

Private equity firms and strategic acquirers favour predictable environments where they can execute integration plans efficiently and generate returns within expected timescales.

Any increase in uncertainty surrounding employment regulation, restructuring flexibility or business taxation is likely to be reflected in acquisition valuations.

Final Thoughts

Valuation in the TPM industry is influenced by far more than revenue growth and EBITDA.

The ability to integrate acquisitions, remove duplication and realise synergies quickly can have a significant impact on what a buyer is willing to pay.

From Baby Blue’s discussions with investors and acquirers, French TPM providers are frequently perceived as being worth around 30% less than comparable UK and US businesses, largely due to labour market rigidity and the challenges associated with post-acquisition restructuring.

Whether that perception is entirely justified is open for debate.

What is clear, however, is that employment regulation plays a far greater role in determining enterprise value than many business owners realise.

For TPM owners considering a future sale, understanding how investors view labour flexibility may prove just as important as understanding revenue growth, customer retention or EBITDA performance.

Lee Bailey and Chris Smith are available to hire on a fractional basis with three and five day due diligence packages available to investors For 2 pm providers, he wants to better understand the market and ensure they don't overpay when performing an acquisition. For a confidential discussion under NDA get in touch.

About the Author

Lee Bailey

Lee Bailey brings 30 years of experience in the IBM services industry, beginning his career in engineering before transitioning into sales and ultimately sales leadership. A qualified Chartered Director (CDir), Lee has served as a Board Member, Director, and Board Advisor for multiple IT services businesses. As the founder of Baby Blue IT & Consulting, he is assembling a team of industry experts focused on IT services and business growth, leveraging his extensive expertise to drive innovation and value for clients.

LinkedIn